ACF2100 Financial Accounting Week 11 Equity Accounting

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

ACF2100 Financial Accounting

Week 11 Equity Accounting

![]() Investments

Investments

Entities often hold equity investments in other entities

– Parent-subsidiary-------consolidation

– Associates and joint ventures------equity method

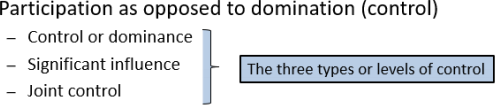

It is the capacity to participate that is required (not actual participation)

Holding 20% or more of the voting power leads to the presumption of significant influence

![]() Associate

Associate

An associate is an entity over which the investor has significant influence

Significant influence is that the power to participate in the financial and operating policy decisions of the investee but is not control or joint control over those policies

![]() Joint ventures

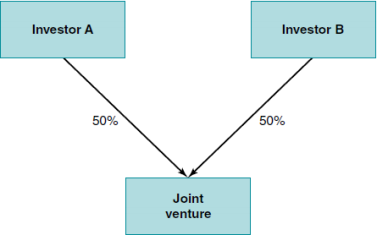

Joint ventures

joint arrangement whereby the parties that have joint control of the arrangement have rights

to the net assets of the arrangement

![]() Equity method of accounting

Equity method of accounting

The asset Investment in Associates and JVs is initially recognized at cost

The asset is subsequently adjusted for the post-acquisition change in the investor’s share of the investee’s net assets

![]() If the investor is not a parent

If the investor is not a parent

– The equity method is applied in the investor’s books

![]() If the investor is a parent

If the investor is a parent

– Cost method is used in the investor’s books

– Equity method is applied on consolidation

– Consolidation worksheet contains:

– Consolidation journals relating to subsidiaries

– Equity journals relating to associates

![]() Example

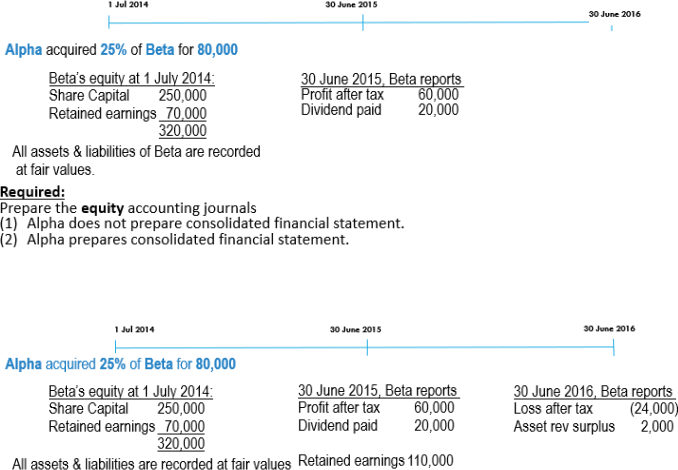

Example

![]() Goodwill and FV adjustments

Goodwill and FV adjustments

The equity method requires adjustments to the investor’s share of post-acquisition equity for:

– Goodwill – this is included in the carrying amount of the investment and cannot be amortised

– Excess (similar to gain on bargain purchase where FVINA > consideration) – must be recognised as income

– Fair value adjustments on acquisition

Appropriate adjustments must be made to investor’s share of the profit or loss after acquisition

Not all recorded profits represent post-acquisition equity

![]() Inter-entity transactions

Inter-entity transactions

Transactions between investor and associate

![]() The investor’s share of any unrealized profits must be adjusted against the share of

The investor’s share of any unrealized profits must be adjusted against the share of

associate profits for the year

– Applies to both upstream and downstream transactions

– Is performed on an after-tax basis

– Adjustments are made to the “Share of P/L of Associates and JVs” and to the “Investment in Associates and JVs”

Relates to unrealised profit…

– in closing inventory

– in opening inventory

– on the transfer of non current assets

A) Where an entity does not prepare consolidated financial statements,

E.g. Assuming Investor acquires 30% shares of Investee

Acquisition Analysis

FVINA=Recorded equity + (1-30%)*BCVR entries-recorded goodwill

FV acquired= FVINA * Investor’s proportional ownership interest

Cost of investment= $XX-cum. Dividend receivable

Goodwill/Gain on bargain= FV acquired – Cost of investment

Journal entries in the accounts of Investor

|

Acquisition Date |

Investment in Associates/JVs |

|

|

|

|

|

|

|

(Acquisition of shares in Investee) |

|

|

|

|

|

|

Current year |

a) Dividend paid/declared |

|

|

|

Cash |

|

|

|

|

Investment in Associates/JVs |

|

|

(Dividend paid: 30% * $XX) |

|

|

|

|

|

|

|

Dividend Receivable |

|

|

|

|

Investment in Associates/JVs |

|

|

(Dividend declared: 30% * $XX) |

|

|

|

|

|

|

|

b) OCI-Asset Revaluation Surplus |

|

|

|

Investment in Associates/JVs |

|

|

|

|

Share of OCI of associates/JVs |

|

|

Share of OCI of associates/JV |

|

|

|

|

Asset Revaluation Surplus |

|

|

(Increase in Asset Revaluation surplus: 30% * $XX) |

|

|

|

|

|

|

|

c) Reported Profit in Investee |

|

|

|

Investment in Associates/JVs |

|

|

|

|

Share of P/L of associates/JVs |

|

|

(Share of profit: 30% * $XX) |

|

|

|

|

|

Adjustment for Profit:

|

Profit for 201x-201x period |

$XX |

|

Pre-acquisition adjustments: |

|

|

Depreciation for Revalued NCA |

($XX) |

|

Post-acquisition profit |

|

|

|

|

|

*Adjustmentsfor inter-entity transactions: |

|

|

Less Unrealised PAT in closing inventory |

|

|

Less Unrealised PAT on sale of NCA in current year |

|

|

Add Realized profit on opening inventory |

|

|

Add Realised PAT on sale of NCA through dep’n in current year |

|

|

|

|

|

Investor’s shares-30% |

$XX |

* Adjusted regardless of whether the transaction is an upstream or downstream one, the others

are same as NCI calculation- step 5

B) Where an entity prepares consolidated financial statements.

Journal entries in consolidated financial statement

|

Acquisition date: |

No entry (avoid double-accounting) |

|

|

|

|

|

|

Current year: |

a) Dividend paid/declared (the only difference) |

|

|

|

Dividend revenue |

|

|

|

|

Investment in Investee |

|

|

|

|

|

|

|

|

|

|

Investment in Investee |

|

|

|

|

Asset Revaluation Surplus |

|

|

|

|

|

|

c) Reported Profit (same) |

|

|

|

Investment in Investee |

|

|

|

|

Shares of P/L of associates/ JVs |

|

|

|

|

|

Previous years: (Period from acquisition to the start of the current year |

||

2023-02-01