BUSI4443/ N14206 CORPORATE FINANCE AUTUMN SEMESTER 2021-2022

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

A LEVEL 4 MODULE, AUTUMN SEMESTER 2021-2022

BUSI4443/ N14206 CORPORATE FINANCE

Question 1.

(a) Capital One will pay a dividend of £60p on its stock. The growth rate in dividends is 5% for first the first three-year period. The dividend growth rate from year 4 to year 6 is 7%, and it is then expected to be a constant 9% per year indefinitely afterwards. The required return on the stock from investors is 14% for the first three years, 17% for the next three years, and 18% afterwards. What is the current stock price for Capital One? [30 marks]

(b) Suppose a five-year bond with a 7% coupon rate and semi-annual compounding is trading for a price of £951.58. Calculate the bond’s yield to maturity (YTM) based on the expression of an annual percentage rate (APR). [20 marks]

(c) Jensen (2004) argues that “…stakeholder theory refuse[s] to specify how to make the necessary tradeoffs among these competing interests, they leave managers with a theory that makes it impossible for them to make purposeful decisions.” Therefore, “…it is logically impossible [for managers] to maximize in more than one dimension, [since] purposeful behavior requires a single-valued objective function.” Critically discuss the views of shareholder value primacy and stakeholder orientation, and does stakeholder orientation benefit for corporate operations? [50 marks] [Total 100 marks]

Question 2.

(a) Mathematically prove the put-call parity. [20 marks]

(b) Assume a stock is currently trading at £50, and in one period the price will either go up by 25% or fall by 13%. If the one-period risk-free rate is 5%, calculate the price of a European put option that expires in one period and has an exercise price of £50?[25 marks]

(c) Malmendier and Tate (2005) investigate the impact of managerial hubris on firm investment by developing an option-based measurement, Holder67. Critically discuss how a CEO could be identified as overconfident using the measurement of Holder67. [25 marks]

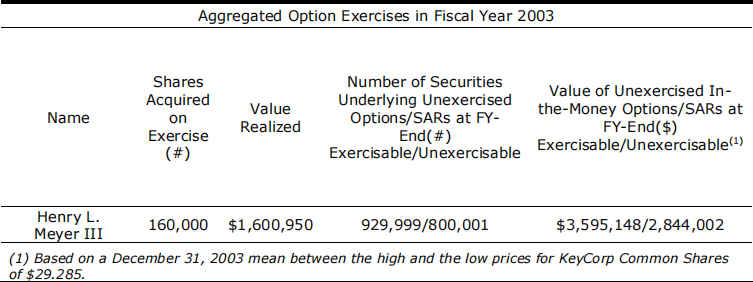

(d) The table below presenting the aggregated option exercises for Henry L. Meyer III, who was the CEO of KeyCorp in 2003. Calculate the average moneyness and explain whether the CEO could be identified as overconfident using Holder67.

[30 marks]

[Total 100 marks]

Question 3.

(a) Where will the following projects plot in relation to the security market line if the

risk-free rate is 6% and the market risk premium is 9%? Which project should be undertaken?

|

Project |

Beta |

IRR |

|

A |

2.00 |

25% |

|

B |

1.60 |

22% |

|

C |

0.80 |

11% |

[15 marks]

(b) Suppose the portfolio constructed by informed traders has a beta of 1.6 and an

expected return of 17%, and the market has an expected return of 12% and the risk-free rate is 5%. Calculate the alpha for the informed investors and explain your findings. [10 marks]

(c) Explain the “homogenous expectations” assumption of CAPM and discuss how this assumption relates to the “real world” investment decision process. [15 marks]

(d) Based on the market efficiency theory, critically discuss the meaning of the term “anomaly” . Provide three examples of market anomalies and explain why each could be considered as an anomaly. [25 marks]

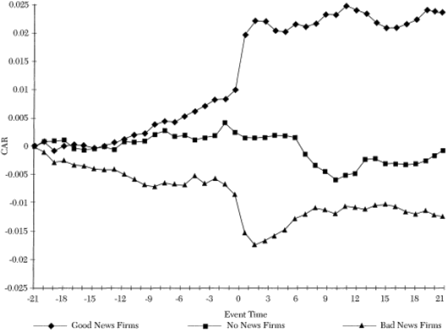

(e) Explain the findings from the graph as shown below, and critically discuss the

main theme and relevant procedure of conducting an event study.

[35 marks]

[Total 100 marks]

Question 4.

(a) What is a firm's weighted average cost of capital if its stock has a beta of 1.38,

Treasury bills yield 6%, and the market portfolio offers an expected return of 16%? In addition to equity, the firm finances 35% of its assets with debt that has a yield to maturity of 7%. The firm is in the 35% marginal tax bracket. [10 marks]

(b) Timeless Limited has issued £15 million in long-term bonds that now have one

year remaining until maturity. The bonds carry an annual coupon rate at 9% and are selling for £971.15 in the market. Meanwhile, the firm’s market value of common equity is £50 million. The tax rate is 35%. For cost of capital purposes, calculate the weight of the debt of the firm and its after-tax cost of debt. [20 marks]

(c) Mayflower Enterprises expected to keep free cash flow in the coming year of £9 million, and such free cash flow is estimated to grow at a rate of 4% per year indefinitely. Mayflower has an equity cost of capital of 12%, a debt cost of capital of 6%, and the corporate tax is 35%. If Mayflower Enterprises maintains a target debt to equity ratio of 0.7. Calculate the value of the firm’s interest tax shield. [15 marks]

(d) In addition to the tax shield offered by the federal government, debt has a lower required rate of return than equity. Why is it not common to observe that have much larger debt components in their capital structure? [20 marks]

(e) Critically discuss and explain the association between stakeholder orientation and leverage.

[35 marks] [Total 100 marks]

Question 5.

(a) Critically discuss whether and how different types of institutional investors may influence corporate governance of their holding firms. [30 marks]

(b) Critically discuss whether improved corporate governance can mitigate the likelihood of managerial overconfidence. [30 marks]

(c) Discuss and explain how the substitution hypothesis between dividends and share repurchases can be empirically tested.

[40 marks]

[Total 100 marks]

Question 6.

A.

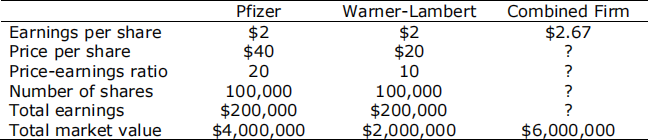

(a) Pfizer plans to acquire Warner-Lambert by making a cash offer of $27 a share for

all 100,000 shares of Warner-Lambert. It estimates that the merger will produce cost savings with a present value of $800,000.

Recently, Warner-Lambert's stock price increased from $20 to $24 per share, evidently due to its excellent financial performance. However, the CFO suggests a revaluation of the offer, pointing out that the true stand-alone value of Warner- Lambert may be $20 per share, not $24 per share. If the stand-alone value is $20 per share, will the merger still generate positive NPV for Pfizer? [10 marks]

(b) Suppose that just before Pfizer and Warner-Lambert’s merger announcement we

observe the following:

Assume merging the two would allow cost savings with a present value $25 million.

i. Pfizer intends to pay $65 million cash for Warner-Lambert. What is the cost?

ii. What is the cost of cash offer if the Warner-Lambert’s share price has already risen by $12 because of rumours that Warner-Lambert might get a favourable merger offer?

iii. Suppose that Pfizer offer 0.325 million shares, what is the apparent cost? What is the true cost? [30 marks]

(c) You are given the following facts:

Assume there is no gains from merging. Pfizer uses its shares to acquire Warner-Lambert.

i . Domdl??? ?u? eqov? ?eql? }oJ ?u? m?J6?p }iJm .

ii . Wue? is ?u? sueJ? ?xDuen6? Je?iol

iii . Wue? is ?u? Dos? o} m?J6?J ?o d}iz?Jl [30 marks]

B. Den e ?eJ6?? Domdeny po eny?uin6 ?o dJ?v?n? e ?e入?ov?Jl Wue? eJ? p?}?nD? m?Duenisms . aisDuss ?u? veJious ?yd?s o} p?}?nD? m?Duenism . [30 marks]

2023-01-19